Down Payment Assistance Continues to Expand in Q1 2026, Reaching 2,679 Programs Nationwide

DPR’s Q2 2024 Homeownership Program Index (HPI) Report, which highlights the homebuyer assistance programs available each quarter to help make homeownership more accessible, has revealed some exciting findings. First, there are now more programs than ever with 2,415 currently being tracked by DPR, plus we’ve noted there are more program resource agencies, with 29 added in Q2 2024, totaling 213 more than we had in our database at this time last year.

Derived from our comprehensive DOWN PAYMENT RESOURCE® database, the HPI report highlights the latest trends in down payment assistance (DPA) programs.

Forty-two homebuyer assistance programs were added in Q2, for a total of 2,415 programs. That’s 213 more programs than a year ago, an increase of 11% — the largest annual jump since DPR began reporting on this data in Q3 2020. Along with the increase in programs came an increase in agencies supporting them, which grew from 1,273 last quarter to 1,302 in Q2 2024.

Our Q2 2024 edition of the report reveals an increase in the availability and diversity of DPA programs, including a new breakdown of the 724 programs that allow for the purchase of multifamily properties. Of those, we found 724 allow for two-unit properties, 491 allow for three-unit properties and 466 allow for four-unit properties.

While 2,193 programs have income limits, 222 do not, a 27% increase from a year ago.

The number of programs offered in Q2 2024 increased by 42 over the previous quarter, raising the total number of programs to 2,415.

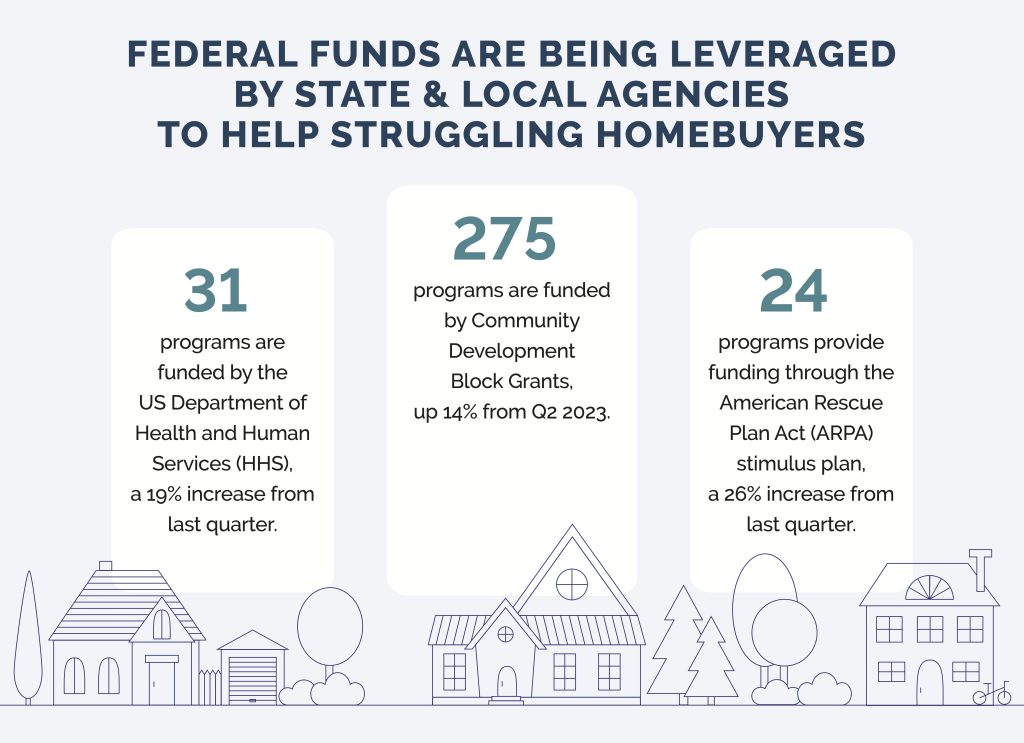

Program spotlight: New Bedford, MA’s Office of Housing and Community Development has enhanced its first-time homebuyer program with ARPA funds to provide first-time buyers with up to $25,000 in down payment and closing cost assistance, with additional funds available for New Bedford city employees.

Program spotlight: The Homeport & Federal Home Loan Bank (FHLB) of Cincinnati – Rise Up Program offers first-generation buyers a $25,000 Grant with a five-year retention agreement. Buyers must self-certify that they are a first-generation homebuyer because either their custodial parent(s) and/or legal guardian(s) have never owned a home in the United States, or the applicant was in the foster care system. The grant may be combined with other local, state and federal funding sources and with the FHLB Cincinnati’s Community Investment Cash Advance Programs.

Program Spotlight: The Broward County Homebuyer Purchase Assistance (HPA) Program in Florida is a first-come, first-served program with limited funding. The program offers up to $80,000 in the form of a deferred 15-year forgivable loan on existing or new construction properties purchased with fixed-rate 15 or 30 year mortgages. Household income must be at or lower than 80% of HUD’s AMI. Funds can be used toward down payment, closing costs, a permanent rate buydown, MI premiums, UFMIP and guarantee fees.

Program spotlight: The Texas State Affordable Housing Corporation offers Mortgage Credit Certificates (MCCs) for first-time and repeat buyers purchasing an existing two, three- or four-unit property provided one of the units will be occupied by the borrower and the property has been occupied for residential purposes for at least five years. Eighty-five programs in DPR’s database are MCC programs, offering a federal tax credit that helps first-time homebuyers with low or moderate incomes pay a portion of their mortgage interest, up to a maximum of 20%.

Here is a breakdown of the homebuyer assistance programs added since Q1 2024 by assistance type:

Overall, the breakdown of homebuyer assistance programs available by type was virtually the same as the previous quarter.

A complete, state-by-state list of homebuyer assistance programs can be viewed here. You can also download the full infographic.

Down Payment Resource builds tools that help mortgage lenders, real estate agents, multiple listing services and consumer listing sites build relationships with homebuyers by connecting them with the homebuyer assistance they need.

To learn how Down Payment Resource can help you support homebuyers, contact us.

Methodology

Published quarterly, DPR’s HPI surveys the funding status, eligibility rules and benefits of U.S. homebuyer assistance programs administered by state and local housing finance agencies, municipalities, nonprofits and other housing organizations. DPR communicates with over 1,300 program providers throughout the year to track and update the country’s wide range of homeownership programs, including down payment and closing cost programs, Mortgage Credit Certificates (MCCs) and affordable first mortgages, in the DOWN PAYMENT RESOURCE® database.