Down Payment Assistance Isn’t a Last Resort—It’s a Smart Financial Strategy

Down Payment Resource (DPR) has released its Q1 2026 Homeownership Program Index (HPI), showing continued growth in homebuyer assistance programs as affordability challenges persist across the housing market.

As of April 1, 2026, there are 2,679 homebuyer assistance programs available nationwide, up from 2,619 in the previous quarter. This steady increase reflects ongoing efforts by housing agencies, nonprofits and local governments to expand access to homeownership and meet evolving borrower needs.

With home prices elevated and buyers facing significant upfront costs, down payment assistance (DPA) continues to play a central role in helping lenders qualify mortgage-ready borrowers. Programs provide meaningful financial support that can be used for down payments, closing costs, rate buydowns and more, helping reduce loan-to-value ratios and strengthen borrower profiles.

Recent data shows buyers are spending more than $31,000 beyond the down payment, underscoring the importance of solutions that preserve liquidity and reduce financial barriers to entry.

Of the 2,679 programs tracked in Q1, 2,073 (77%) are currently active and funded, providing immediate opportunities for homebuyers across the country.

Municipalities continue to lead in program delivery, accounting for 39% of all programs, followed by nonprofits at 22% and state housing finance agencies at 18%. This strong local presence reflects the importance of community-based solutions in addressing affordability challenges at the regional level.

This level of availability ensures that lenders have a wide range of tools to help borrowers move forward, even in a challenging market.

Programs continue to expand in ways that reflect how today’s buyers are approaching homeownership.

Support for first-time buyers remains strong, with 1,666 programs (62%) available to those entering the market. First-generation buyer programs also remain steady, helping expand access for households without a history of homeownership.

In addition, 284 programs (11%) have no income limits, giving lenders more flexibility to qualify a broader range of borrowers, including those in the “missing middle” who may earn too much for traditional assistance but still face affordability constraints.

Alaska Housing Finance Corporation’s (AHFC) First Home Program offers a first mortgage loan with no income or sales price limits. Buyers can purchase a single-family home, duplex, condo, townhome/PUD, manufactured home or modular home. To qualify as a “first time homebuyer,” borrowers may not have owned a primary residence in the past three years.

Homebuyer assistance programs are also evolving to support a wider range of housing choices. A total of 934 programs (35%) now allow purchases of multi-unit properties (2–4 units), up from 923 in the previous quarter. These options can help buyers offset costs through rental income while building long-term wealth.

At the same time, 1,053 programs (39%) support manufactured housing, up from 1,041 in Q4. Manufactured homes remain one of the most affordable housing options available, making them an increasingly important pathway to homeownership.

Your Turn Homebuyer Assistance from New Hampshire Community Loan Fund offers up to $35,000 toward the down payment and/or closing costs for a manufactured home. Current ownership is allowed, and there are no sales price limits. Incomes can be 100% HUD Area Median Income (AMI). Buyers can qualify for an additional $35,000 loan if they buy a new Energy Star home.

The structure of homebuyer assistance programs continues to reflect a wide range of borrower needs.

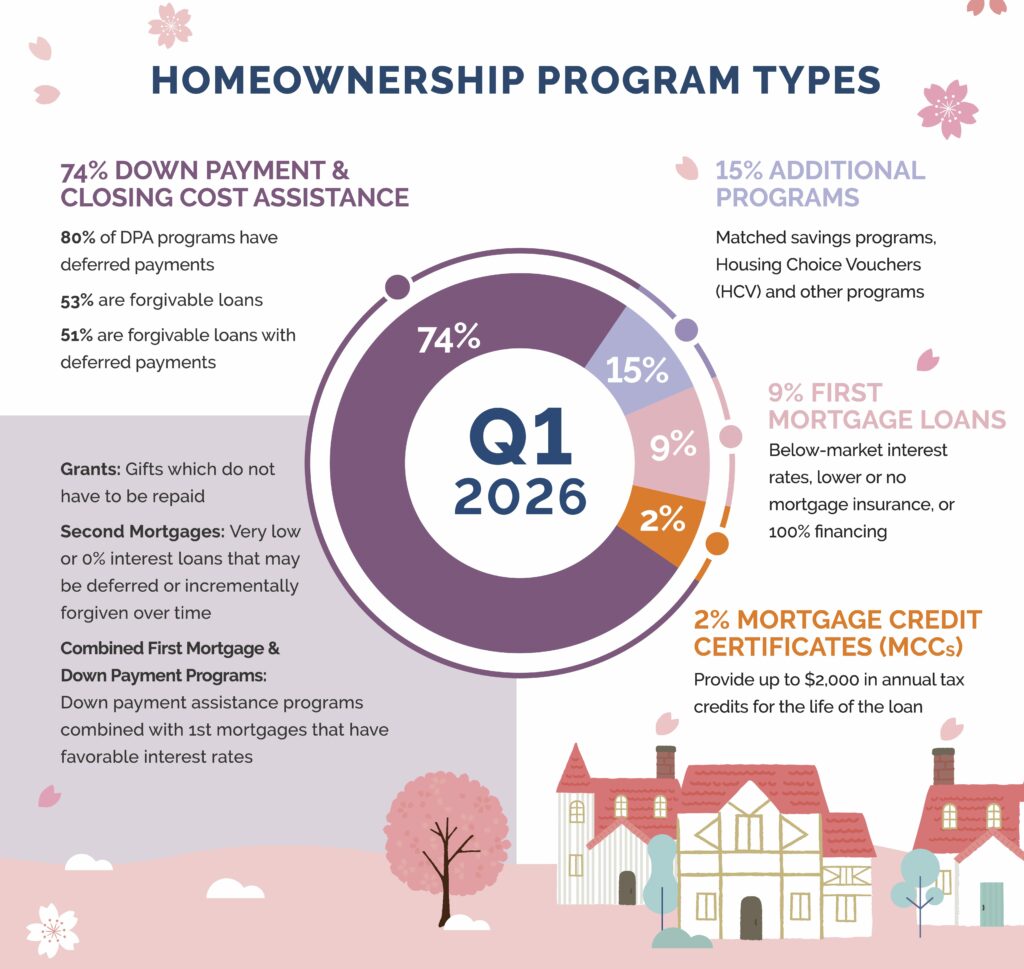

Second-mortgage programs remain the most common, accounting for 56% of all programs. These are often structured as deferred or forgivable loans, reducing upfront costs and easing the path to homeownership.

Combined assistance programs represent 10% of offerings, blending first mortgages with additional support, while first-mortgage programs account for 9%. Grants make up 8% of programs and remain especially valuable because they do not require repayment.

Other program types—including resale-restricted housing, housing choice vouchers, matched savings and mortgage credit certificates—provide additional ways to improve affordability and expand access.

Targeted incentive programs continue to play an important role in expanding access to homeownership.

A total of 206 programs offer special incentives based on occupation or borrower characteristics, up from 201 in the previous quarter. These include programs supporting educators, Native American homebuyers, Veterans and protectors such as law enforcement and first responders.

Down Payment Assistance from the City of New Haven (CT) offers residents up to $20,000 in the form of a zero (0%) interest five-year forgivable loan. Municipal employees, teachers, firefighters, military or police officers can qualify for an additional $2,500. Income can be up to 120% AMI, and the funds can be used for a single-family or multifamily (1-4 units) purchase.

Here is a breakdown of the homebuyer assistance programs as of Q1 2026 by assistance type:

The majority of programs, 1,499 (56%), are second-mortgage programs, up from 1,461 in the previous quarter. A second mortgage DPA, often provided by a state housing finance agency (HFA), local government or nonprofit organization, is a subordinate loan recorded after the first mortgage. 274 programs (10%) are combined assistance programs, while 245 (9%) are first-mortgage programs, both holding relatively steady quarter over quarter. 220 programs (8%) are grants, up from 207 in Q4, offering non-repayable assistance that continues to grow in availability.

Other program types include 143 BMR/resale-restricted programs (5%), 92 housing choice voucher programs (3%), 63 matched savings programs (2%) and 49 mortgage credit certificates (2%), reflecting a range of approaches to improving affordability and expanding access to homeownership.

The overall composition of homebuyer assistance programs remained stable in Q1, with most programs active and focused on down payment and closing cost support.

Of the 2,679 homebuyer assistance programs nationwide:

Homebuyers are encouraged to use DPR’s free search tool to find programs for which they may qualify.

A complete, state-by-state list of homeownership programs can be viewed here. You can also download the full infographic.

Down Payment Resource builds tools that help mortgage lenders, real estate agents, multiple listing services and consumer listing sites build relationships with homebuyers by connecting them with the down payment help they need.

To learn how Down Payment Resource can help you support homebuyers, contact us.

Methodology

Published quarterly, DPR’s HPI surveys the funding status, eligibility rules and benefits of U.S. homebuyer assistance programs administered by state and local housing finance agencies, municipalities, nonprofits and other housing organizations. DPR communicates with over 1,400 program providers throughout the year to track and update the country’s wide range of homeownership programs, including down payment and closing cost programs, Mortgage Credit Certificates (MCCs) and affordable first mortgages, in the DOWN PAYMENT RESOURCE® database.