85% of Homeowners Wish They Had Known These Things Before Buying

Buying a home is likely the biggest purchase you’ll make in your lifetime. There’s a reason why people joke they feel “house poor” when they leave the closing table. Too often the burden of the down payment leaves homebuyers’ cash reserves empty.

And, new data shows that can be a recipe for financial stress.

Research by the JPMorgan Chase Institute flips the script on homebuyer risk. It turns out that having a cash cushion trumps a big down payment.

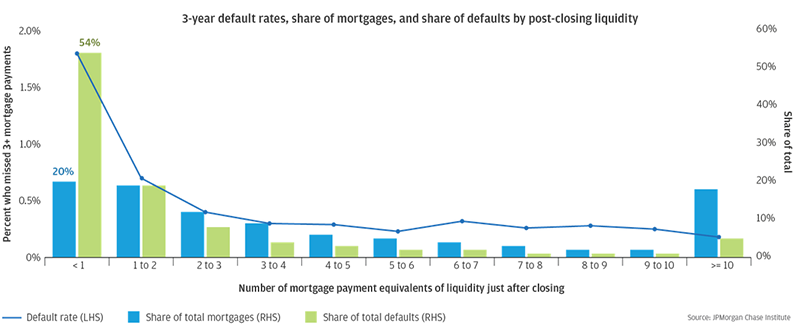

Historically, a big down payment is associated with lower risk, but the report found that liquidity — having at least three months of mortgage payments available — is a better measure of homeownership success. In fact, borrowers with less than one month of mortgage payment reserves defaulted at a rate five times higher than borrowers who had three and four months of mortgage payments available.

Homebuyers have an incentive of securing a lower interest rate to try and stretch to make a larger down payment. But, is it really the best for long-term success?

The short answer is no. Don’t make a big down payment at all costs.

The report found that borrowers with little liquidity but more equity (made a larger down payment) defaulted at considerably higher rates than borrowers with more liquidity but less equity (made a smaller down payment). Further, default was preceded by a drop in income regardless of the homeowner’s equity, income level, or payment burden.

The report’s findings suggest that a policy or program encouraging borrowers to make a slightly smaller down payment and use the residual cash to fund an “emergency mortgage reserve” account might lead to lower default rates.

The good news is that many down payment assistance programs available today can help you do just that. You may be able to combine an affordable first mortgage with a down payment assistance program. It can help you to come to the closing table without wiping out your bank account.

That’s good news for homebuyers and the mortgage industry.

Before you assume a big down payment is best, research your down payment options and talk to your lender and real estate agent.

Never want to miss a post? For more useful down payment and home buying information, subscribe to our mailing list.