85% of Homeowners Wish They Had Known These Things Before Buying

File this question under “it depends.”

It’s true that loans with down payments of 20 percent or more cost borrowers less over time than low down payment loans. Low down payments leave larger principals to pay off, and those principals create more interest over time. Low down payment loans also require mortgage insurance.

However, a low down payment itself can actually boost affordability by getting you off the sidelines and into a home of your own sooner.

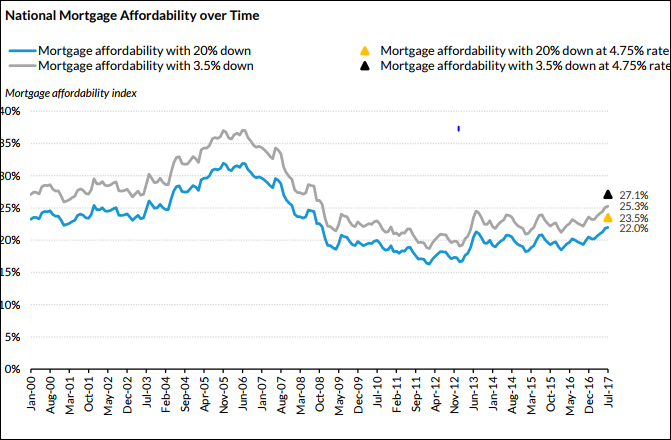

At current interest rates and based a median family income, you’d need about 22 percent of your income for monthly payment with a 20-percent-down mortgage and about 24 percent with a 3.5 percent down payment. And, should rates rise to 4.75 percent by the end of this year, a buyer putting 20 percent down would pay about 25 percent of his monthly income and a buyer using a low-down payment loan at 3.5 percent down payment would pay about 28 percent of the buyer’s monthly income.

While 20 percent isn’t necessary and isn’t even the average (7.6 percent), it will help reduce the monthly payment simply because your total mortgage loan is less than with a lower down payment. But, it’s important to evaluate the cost-benefit of a lower down payment.

Forgoing a low down payment today to save for a 20 percent down payment in the future changes the equation for first-time buyers. With home prices and rates on the rise in 2018, affordability will likely worsen in the months ahead.

In fact, a recent survey by Apartment List found that it takes many millennials a decade or more to save enough to make a 20 percent down payment. By that time, the costs of waiting so long will outweigh the advantages of a larger down payment.

Since 2012, it has been cheaper to buy than rent in most markets and rents today are consuming an even larger share of monthly disposable income. By the end of this year, rates could rise as high as 4.75 percent, and prices are forecasted to continue to rise in 2018. Rising rates and prices will increase the cost of a 20 percent down payment for those who delay.

In the Barriers to Accessing Homeownership study released in November, analysts at the Urban Institute’s Housing Finance Policy Center concluded that “with rising home prices and interest rates, access to sustainable mortgage credit is often only possible with low–down payment loans.”

For more data and information on down payment trends from a variety of sources, subscribe to our monthly Down Payment Report.