85% of Homeowners Wish They Had Known These Things Before Buying

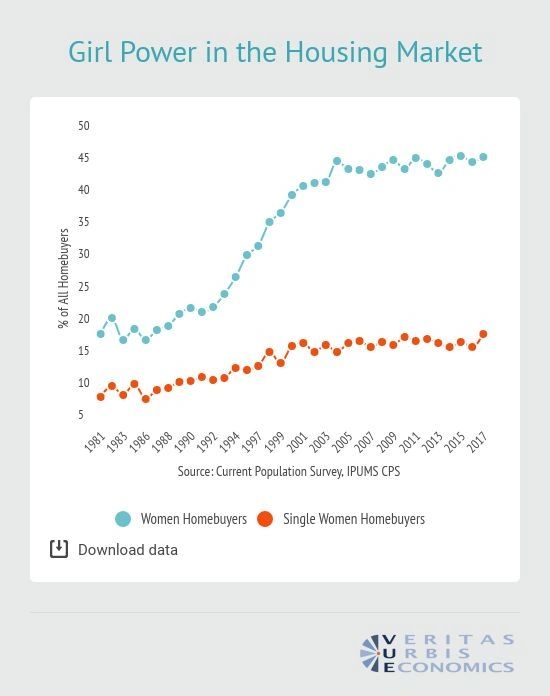

Who’s buying homes these days? According to a new report, it’s all the single ladies. Veritas Urbis Economics took a look at the demographic changes in homebuyers since 1981 and, like a lot of things since the 80s, it looks quite different today.

The share of U.S. homebuyers comprised of women increased to 46.4% in 2017 from just 18.9% in 1981. What’s more, the share of homebuyers that are single women is at an all-time high, rising to 18.9% in 2017 from just 9.1% in 1981. The increase in women homebuyers is a result of huge gains in the share of women with bachelor’s degrees, increased earning power and a growth of female-headed households — both alone and with partners.

Another big change since the 80s is the jump in share of buyers over age 55 — increasing to 27.8% in 2017 from just 16.1% in 1981. That’s an almost 73% jump. On the other hand, the share of homebuyers that are under 35 years old is at an all-time low, falling to 33.7% in 2017 from a high of 52% in 1981.

In the past, having a child was a key driver for buying a home, but this report shows that homebuyers in the U.S. are increasingly without children and alone. The share of buyers with children fell to an all-time low of 40.7% in 2017, down from 51.4% in 1981. Furthermore, the share of all homebuyers made up of single-person households has increased to 21.2% in 2017 from 15.3% in 1981.

Use these four tips from Credit.com to increase your odds of success.