Five Myths About Women Homebuyers and What the Data Really Shows

Down Payment Resource (DPR) has just released its Q2 2025 Homeownership Program Index (HPI) report documenting a continued rise in the number of available and funded homebuyer assistance programs from April to June 2025.

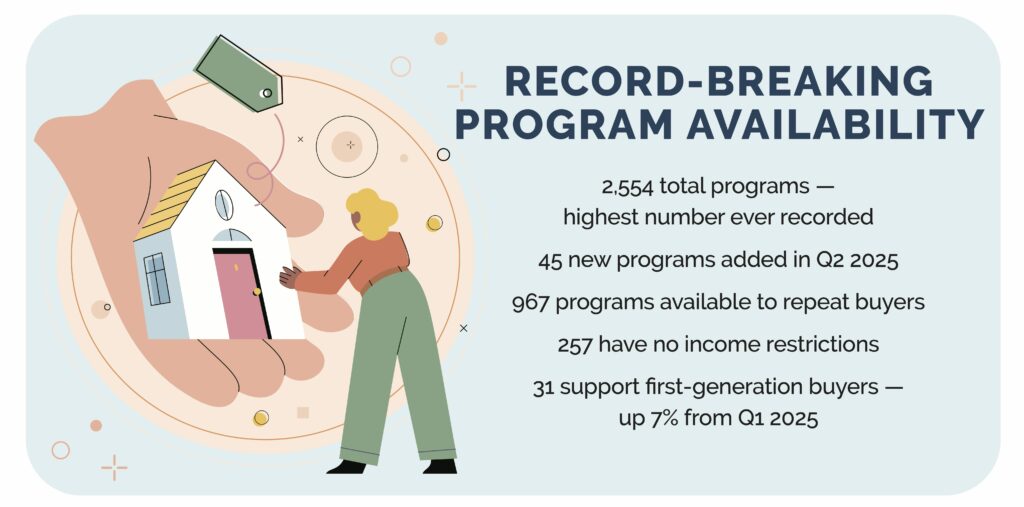

45 programs were added during the quarter, for a total of 2,554 — the highest number of programs DPR has recorded. Additionally, the data revealed that 967 programs (38%) are available to repeat buyers; 257 programs (10%) do not have income restrictions, increasing the number of buyers who might qualify for assistance; and 31 programs support first-generation homebuyers, an increase of 7% over the last quarter.

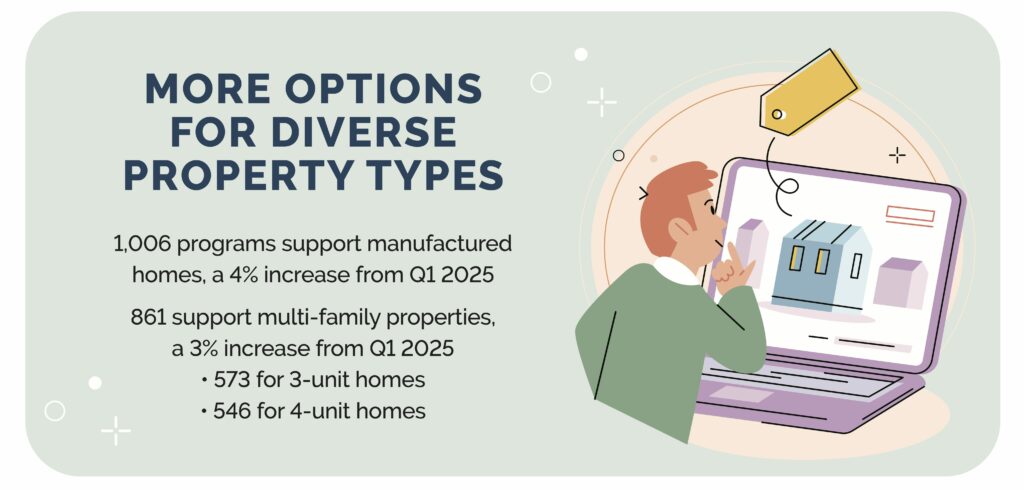

The Q2 report also shows a growing number of programs to support the purchase of manufactured and multi-family homes, allowing borrowers to access more affordable housing and housing that will provide a passive income. A total of 861 programs now support multi-family purchases, a 3% increase over Q1 2025. Of these, 573 allow for 3-unit properties, up 2% from Q1 2025, while 546 allow for four-unit properties, up 2% from the previous quarter.

Likewise, the number of programs allowing for the purchase of manufactured housing has increased from 971 in Q1 2025 to 1,006 in Q2 2025, a 4% increase.

The report also reveals a program-type mix showing little change this quarter, with below-market rate (BMR)/resale restricted, grants, and second mortgages making quarterly gains. Slightly more programs are reserved for first-time buyers, moving from 1,557 in Q1 2025 to 1,587 in Q2, a 3% increase.

Derived from our comprehensive DOWN PAYMENT RESOURCE® database, the HPI report highlights the latest trends in down payment assistance (DPA) programs. On average, these programs can lower a buyer’s LTV by 6%, helping more applicants qualify for a mortgage.

The number of programs offered in Q2 2025 increased by 45 over the previous quarter, raising the total number of programs nationwide from 2,509 to 2,554—the highest total ever recorded by DPR, widely considered the OG of DPA. Of these:

Program spotlight: The Housing Resources of Western Colorado Purchase Assistance Loan program provides qualifying homebuyers in Mesa and Garfield counties with up to $65,000 in the form of a 30-year deferred loan with no monthly payments; however, repayment becomes due at mortgage pay off, sale of the house or change in the borrower’s primary residence. Applicants can be repeat buyers with incomes of up to 120% of the HUD Area Median Income (AMI).

Program spotlight: The SECURA Employer Assisted Housing Grant, administered by Appleton Housing Authority (AHA) in Appleton, Wisconsin, offers a conditional grant of up to $5,000 to first-time homebuyers. The grant, available for purchasing homes nationwide, will be forgiven as long as the applicant remains at SECURA, a regional insurance company that provides property and casualty insurance in 13 states, for a full five years after closing.

First-generation homebuyers are the first in their family (or in this country) to purchase a home.

Program spotlight: The City of Eden Prairie First Generation Homebuyer Program offers $3,000-$40,000 to first-time and first-generation homebuyers. (Buyers must sign an attestation to affirm they have never owned a home previously nor have their parents.) The funds can be used for up to 50% of a down payment; up to 100% of closing costs (not to exceed $7,500); or to reduce the mortgage principal up to 15% of the purchase price. There is a 30-year balloon payment; however, OHCS may waive the repayment if the homeowner can prove financial hardship. Income can be up to 100% of HUD AMI.

Of these, 68 offer assistance for educators, 52 to Native Americans, 45 to military Veterans, and 35 to active-duty military. It’s important to note that these buyers can also qualify for many of the other 2,554 programs in the Down Payment Resource database.

Program spotlight: Community Connection of Northeast Oregon Veteran Down Payment Assistance Loan Program offers up to 20% of the purchase price of a home or $30,000 to Veterans living in Oregon who are first-time homebuyers in Baker, Grant, Union or Wallowa counties. Funding is in the form of a deferred 0% 5-year forgivable loan and the buyer’s income must be within 100% AMI or lower.

A repeat homebuyer has previously owned a home and is now purchasing another home. This is in contrast to a first-time homebuyer, which HUD defines as someone who has not owned a home in the past three years.

This latitude may make it easier for lenders to qualify buyers at moderate income levels who need help with their down payment, closing costs, or other costs of homeownership.

There was also an uptick in statewide programs in Hawaii, Missouri, Oklahoma, Pennsylvania and Virginia.

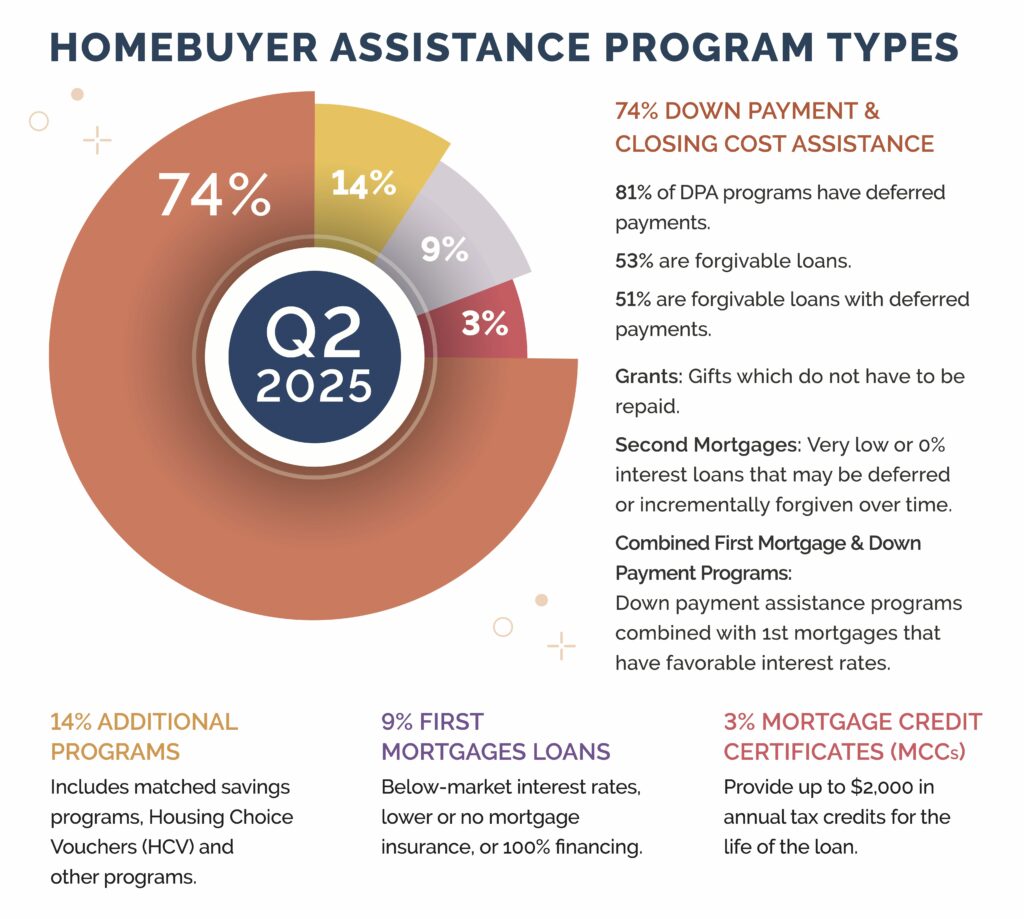

Here is a breakdown of the homebuyer assistance programs added since Q1 2025 by assistance type:

Overall, the breakdown of homebuyer assistance programs available by type changed slightly from the previous quarter.

A complete, state-by-state list of homebuyer assistance programs can be viewed here. You can also download the full infographic.

Down Payment Resource builds tools that help mortgage lenders, real estate agents, multiple listing services and consumer listing sites build relationships with homebuyers by connecting them with the homebuyer assistance they need.

To learn how Down Payment Resource can help you support homebuyers, contact us.

Methodology

Published quarterly, DPR’s HPI surveys the funding status, eligibility rules and benefits of U.S. homebuyer assistance programs administered by state and local housing finance agencies, municipalities, nonprofits and other housing organizations. DPR communicates with over 1,300 program providers throughout the year to track and update the country’s wide range of homeownership programs, including down payment and closing cost programs, Mortgage Credit Certificates (MCCs) and affordable first mortgages, in the DOWN PAYMENT RESOURCE® database.