The Down Payment Resource Q4 2023 Homeownership Program Index Report

January 30, 2024

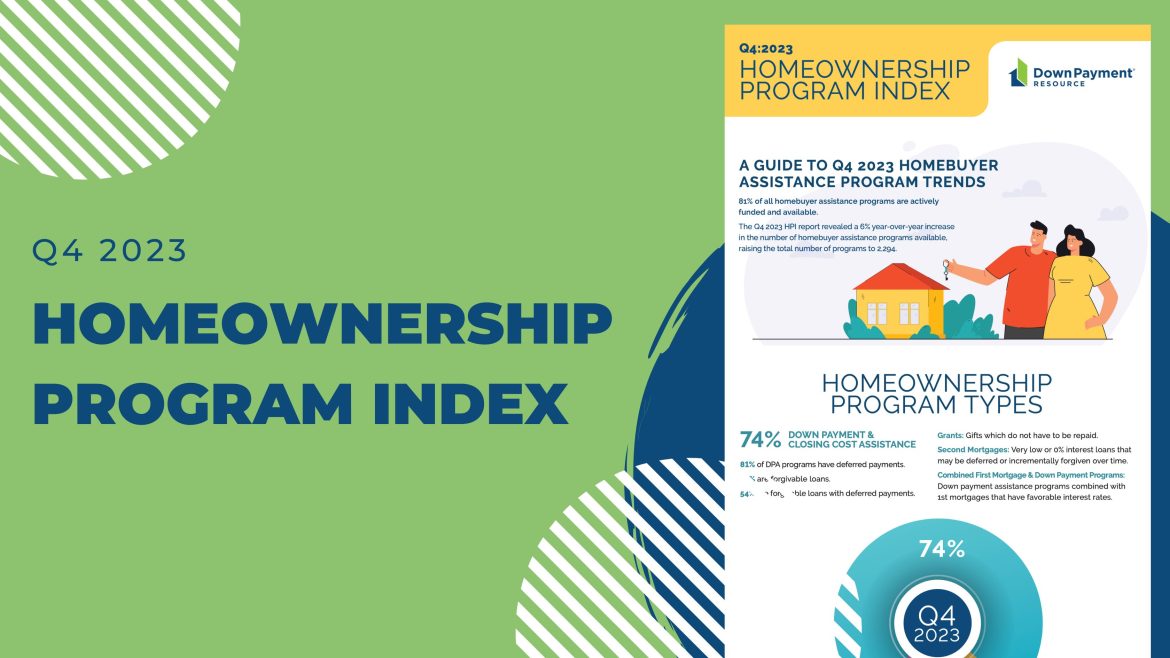

In an era marked by unprecedented challenges in housing affordability, we’ve published our Q4 2023 Homeownership Program Index (HPI) Report to highlight the homebuyer assistance programs available to help make homeownership more accessible. Derived from our comprehensive DOWN PAYMENT RESOURCE® database, this report highlights the latest trends in down payment assistance (DPA) programs in 2023.

Our Q4 2023 edition reveals an increase in the availability and diversity of DPA programs, including an increase in programs supporting the purchase of manufactured and multi-family homes and the evolving dynamics of Mortgage Credit Certificate (MCC) programs. Read on to explore how DPA is evolving in the U.S.

Program Trends

The number of programs offered in Q4 2023 increased by 135 over the previous year, raising the total number of programs to 2,294.

804 programs allow for the purchase of a manufactured home, up 20% from the previous year. According to the Manufactured Housing Institute, an industry advocacy group, the average cost of a manufactured or mobile home is $127,250 or $85/square foot, while the average cost of a site-built home is $413,160 or $167.87/square foot. Depending on the local housing market, that can make a big difference. In California, for example, nearly half (47%) of manufactured housing is affordable to very low-income households, compared to just 18% of the state’s housing stock overall. Because manufactured housing opens up homeownership to many low- and moderate-income buyers, we think this trend will pick up speed in the coming years. And if you’re wondering if mobile homes and manufactured homes are the same thing — yes, they are. According to HUD, a factory-built home prior to June 15, 1976, is a mobile home and one built after June 15, 1976 is a manufactured home.

Program spotlight: The City of Napa (CA) offers a down payment assistance program specifically for buyers of a mobile or manufactured home who are first-time homebuyers. The program offers buyers up to $58,000 or 30% of the purchase price, whichever is less, and is in the form of a 20-year deferred, forgivable loan. The buyer’s income needs to be 80% or less of the Area Median Income (AMI), which for Napa in 2022 (the most recent year available) was $105,809.

686 programs allow for the purchase of a multi-family property, up 8% from the previous year. Using DPA to purchase a multi-family property has become a very hot topic lately, and about 30% of the programs in DPR’s database allow funds to be used for a multi-family investment (1-4 units). Typically, the buyer must reside in one of the units but can rent the others, allowing them to be both a buyer and an investor. These assistance programs often require the borrower to complete homeownership and landlord-prep classes, which we think will help ensure long-term stability for new homeowners.

Program spotlight: The City of Chicopee (MA) funds a multifamily incentive program that pays $16,000 toward a buyer’s down payment or closing costs to purchase a multi-family (three rental units and the owner’s unit) property within the city. The loan is structured as a 16-year forgivable loan with $1,000 forgiven annually.

78 programs are mortgage credit certificate (MCC) programs, a 19% drop from the previous year. The MCC program is a homebuyer assistance program designed to help lower‐income families afford homeownership. The program allows homebuyers to claim a dollar‐for‐dollar tax credit for a portion of mortgage interest paid per year, up to $2,000. The remaining mortgage interest paid may still be calculated as an itemized deduction. MCC programs were highly popular up until about 2020, when our data showed a cooling off as state housing finance agencies have exceeded their capacity to offer the bond-funded MCC programs or don’t want to handle them administratively.

Breakdown of New Programs

Here is a breakdown of the homebuyer assistance programs added since Q4 2022 by assistance type:

Rehab assistance programs saw the largest YoY growth, rising 300% since the same quarter in 2022.

Below market value (BMR)/resale restriction programs saw the second largest growth with a rise of 112%.

Matched savings programs rose 34%.

Grant programs rose 13%.

Breakdown of All Programs

Overall, the breakdown of homebuyer assistance programs available by type was virtually the same as the previous quarter.

Of the 2,294 homebuyer assistance programs:

81% of programs are currently funded.

9% of programs are currently inactive.

4% of programs have a waitlist for funding.

6% of programs are temporarily suspended.

74% of programs in the database are for down payment or closing cost assistance.

10% of programs are first mortgages.

3% of programs are Mortgage Credit Certificates (MCCs).