Down Payment Assistance Continues to Expand in Q1 2026, Reaching 2,679 Programs Nationwide

Down Payment Resource has just released its Q4 2024 Homeownership Program Index (HPI) Report, which shows a continued rise in the number of available homebuyer assistance programs from last quarter. There are now 22 new programs for a total of 2,466 – the highest number of programs we’ve ever recorded. Since Q4 2023, 172 new programs have been added, a 7% YoY increase.

Derived from our comprehensive DOWN PAYMENT RESOURCE® database, the HPI report highlights the latest trends in down payment assistance (DPA) programs. On average, these programs can lower a buyer’s LTV by 6%, helping more applicants qualify for a mortgage.

The Q4 report also shows a growing number of programs to support the purchasing of manufactured and multi-family homes, allowing borrowers to access more affordable housing and housing that will provide a passive income. A total of 805 programs now support multi-family purchases, a 17% increase over Q4 2023’s 686 programs, a 17% YoY increase. Of these, 539 allow for 3-unit properties, up 2% from Q3 2024, while 513 allow for four-unit properties, up 3% YoY.

Likewise, the number of programs allowing for the purchase of manufactured housing has increased from 804 in Q4 2023 to 914 in Q4 2024, a 14% increase.

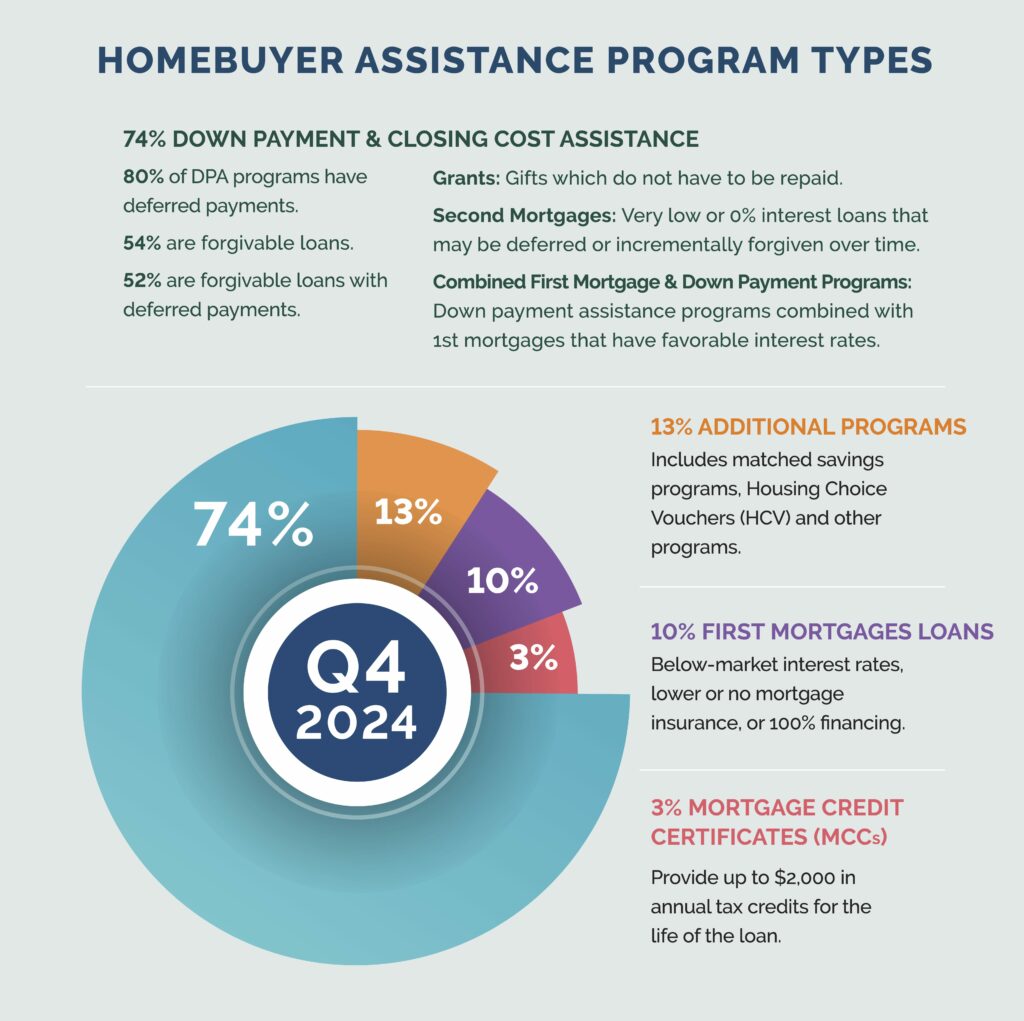

The report also reveals a slight shift in program types, second mortgages, below market rate (BMR)/resale restricted, combined assistance and grant programs making YoY gains. There was also an increase in the number of local housing finance agencies offering programs, from 99 in Q4 2023 to 171 in Q4 2024, a 60% YoY increase.

Slightly more programs are being reserved for first-time buyers, moving from 1,381 in Q4 2023 to 1,518 in Q4 2024, a 10% YoY increase.

The number of programs offered in Q4 2024 increased by 22 over the previous quarter, raising the total number of programs to 2,466 from 2,444.

Program spotlight: The City of San Antonio Homeownership Incentive Program offers up to $15,000 to first-time homebuyers with a household income of $74,350-$140,200 unless displaced involuntarily and permanently moved from real property or if they were someone who owned a home previously, but have since divorced. 75% is forgiven over a ten-year period. 25% would need to be paid back if there is a change in ownership, the home is sold or the loan is refinanced with cash back. The maximum purchase price for an existing home is $305,200 and for new construction $325,800.

Program spotlight: Champlain Housing Trust Manufactured Home Down Payment Loan in Vermont offers up to $40,000 to buyers of manufactured homes in the form of a deferred and assumable second loan until the home is sold, transferred or refinanced. Applicant income must be between $79,800 and $188,400, with no limits on purchase price.

Program spotlight: Atlanta Housing’s Homeownership Down Payment Assistance Program offers up to $20,000 and up to $25,000 for professionals and para-professionals in public safety, healthcare and education; borrowers who are disabled; current military or veteran; and voucher recipients in the form of a 10-year forgivable loan. Borrower income cannot exceed 80% of the average median income for metro Atlanta and the maximum purchase price is $375,000.

Program spotlight: Affordable Housing Partnership Touhey Homeownership Foundation Reparative Justice Housing Fund in New York offers grants up to $10,000 to assist first-time Black homebuyers purchasing a home, with 1-4 units permitted, in the City of Albany, and up to $5,000 if the home is purchased in Rensselaer, Schenectady, Troy or Watervliet. The grant can be used to address a variety of financial barriers to homeownership. There are no Income or purchase price limits.

Here is a breakdown of the homebuyer assistance programs added since Q4 2024 by assistance type:

Overall, the breakdown of homebuyer assistance programs available by type was virtually the same as the previous quarter.

A complete, state-by-state list of homebuyer assistance programs can be viewed here. You can also download the full infographic.

Down Payment Resource builds tools that help mortgage lenders, real estate agents, multiple listing services and consumer listing sites build relationships with homebuyers by connecting them with the homebuyer assistance they need.

To learn how Down Payment Resource can help you support homebuyers, contact us.

Methodology

Published quarterly, DPR’s HPI surveys the funding status, eligibility rules and benefits of U.S. homebuyer assistance programs administered by state and local housing finance agencies, municipalities, nonprofits and other housing organizations. DPR communicates with over 1,300 program providers throughout the year to track and update the country’s wide range of homeownership programs, including down payment and closing cost programs, Mortgage Credit Certificates (MCCs) and affordable first mortgages, in the DOWN PAYMENT RESOURCE® database.