Five Myths About Women Homebuyers and What the Data Really Shows

Down Payment Resource (DPR) has released its Q3 2025 Homeownership Program Index (HPI), revealing another record-setting quarter for homebuyer assistance.

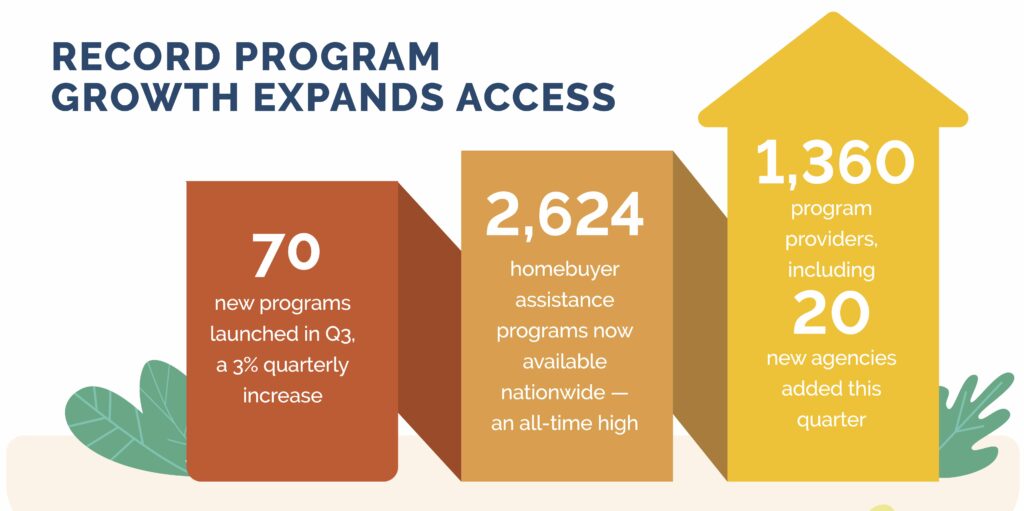

From July through September 2025, 70 new assistance programs were added, bringing the nationwide total to 2,624 — the highest number DPR has ever recorded. Additionally, 20 new program providers were added to DPR’s database during Q3, bringing its provider total to 1,360.

With an average benefit of $18,000, down payment assistance (DPA) remains one of the most essential tools for addressing the nation’s affordability challenges. Programs continue to expand in scope, serving a broader range of incomes, property types and borrower needs, including first-generation, military and repeat buyers.

While the median U.S. home price climbed to $375,000 in Q3 2025, up from $369,000 in the previous quarter, homebuyers saw some relief as the average 30-year fixed mortgage rate dipped from 6.75% in July to 6.26% by mid-September.

Even so, affordability remains a hurdle, and DPA is playing an increasingly important role in helping lenders qualify mortgage-ready buyers. DPR’s data shows that assistance can reduce a borrower’s loan-to-value ratio (LTV) by an average of 6%, improving access to credit and supporting more sustainable lending.

Of the 2,624 available programs, 996 (38%) support repeat buyers and 1,628 serve first-time buyers. Many also make exceptions for military homebuyers, allowing them to be eligible even after previous ownership. A total of 273 (10%) programs have no income limits, expanding access for moderate-income borrowers. Additionally, 32 programs now support first-generation homebuyers, representing a 3% increase over the previous quarter.

Program Spotlight:

The Colorado Housing and Finance Authority (CHFA) FirstGeneration Plus offers buyers up to $25,000 in the form of a 30-year deferred, 0% interest rate loan. All borrowers must be first-time buyers, with at least one being a first-generation buyer. The income limit for this statewide program is $196,140 and the purchase price can be up to $806,500. Borrowers must make a minimum financial contribution of $1,000.

The Family Housing Resources (FHR)/Pima County WISH Down Payment Assistance Program offers up to $32,000 in the form of a five-year forgivable second lien, repayable at 20% per year and can be used for the purchase of a manufactured home provided it’s already on land and affixed. Income can be up to 78% Area Median Income (AMI), with the buyer required to contribute at least $5,000, which can be gifted (but not from the seller). Must be a first-time homebuyer purchasing property in the City of Tucson, Ariz. or Pima County, excluding tribal lands.

More than half of all programs, or 56%, are structured as second mortgages, with most being deferred or forgivable. Another 10% are “combined” programs, which typically blend a first mortgage (usually below market rate) and down payment assistance in the form of a second or grant, or both. 9% of programs are first-mortgage products, and 53% of all down payment assistance offerings provide full or partial forgiveness over time, typically tied to owner-occupancy or primary-residence requirements.

The City of Sunnyvale First Time Homebuyer Down Payment Assistance Loan Program in California offers up to $50,000 in the form of a second mortgage loan to first-time homebuyers who live or work in Sunnyvale and purchase a home within city limits. The buyer’s income can go up to 120% of the AMI for Santa Clara County. Homes may be new or resale single-family homes, town homes, or condominiums. Homebuyer education is required.

203 programs offer special incentives based on occupation or service, including 71 (35%) for educators, 52 (26%) for Native Americans, 50 (25%) for protectors such as law enforcement officers and emergency medical technicians, 49 (24%) for Veterans and 38 (19%) for active-duty military personnel.

The Neighborhood Nonprofit Housing Corporation – Home Choice Program is designed to meet the needs of people with disabilities (or those who have a family member with a disability) as defined by the Americans with Disabilities Act of 1990 or by the Fair Housing Amendment Act of 1988. Households up to 80% HUD AMI can qualify for up to $70,000 in the form of a 30-year, 1% interest, amortizing second mortgage with no prepayment penalty to purchase a home in the state of Utah. The homebuyer(s) must contribute a minimum of $500 toward the purchase.

Here is a breakdown of the homebuyer assistance programs added since Q2 2025 by assistance type:

Overall, the breakdown of homebuyer assistance programs available by type changed slightly from the previous quarter.

A complete, state-by-state list of homebuyer assistance programs can be viewed here. You can also download the full infographic.

Down Payment Resource builds tools that help mortgage lenders, real estate agents, multiple listing services and consumer listing sites build relationships with homebuyers by connecting them with the homebuyer assistance they need.

To learn how Down Payment Resource can help you support homebuyers, contact us.

Methodology

Published quarterly, DPR’s HPI surveys the funding status, eligibility rules and benefits of U.S. homebuyer assistance programs administered by state and local housing finance agencies, municipalities, nonprofits and other housing organizations. DPR communicates with over 1,300 program providers throughout the year to track and update the country’s wide range of homeownership programs, including down payment and closing cost programs, Mortgage Credit Certificates (MCCs) and affordable first mortgages, in the DOWN PAYMENT RESOURCE® database.