Down Payment Assistance Continues to Expand in Q2 2026, Reaching 2,746 Programs Nationwide

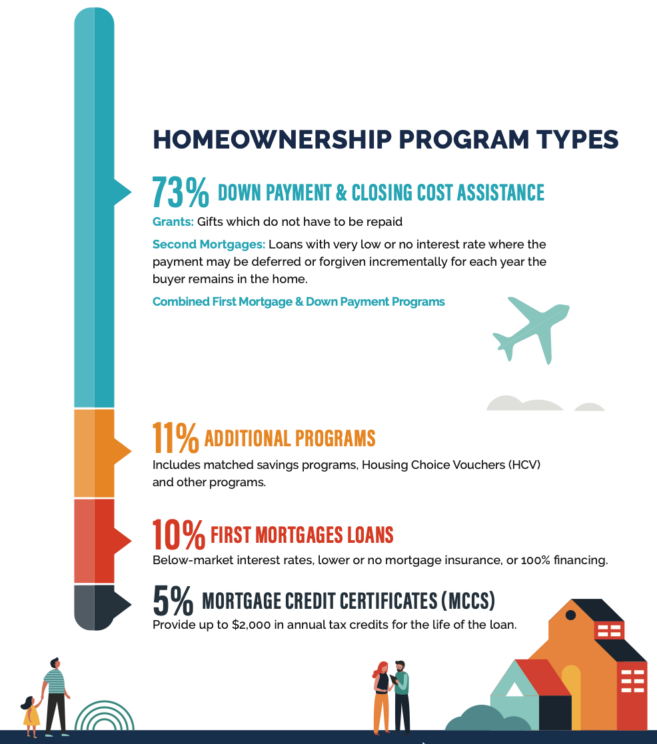

The Second Quarter 2021 Homeownership Program Index (HPI) reveals that Down Payment Assistance (DPA) programs make up 73 percent of the programs in the Down Payment Resource database.

These programs may come in the form of a repayable second mortgage loan or a non-repayable grant. They’re offered by federal, state, county or local government agencies, nonprofits or employers, and they’re available across the country for income- and credit-qualified buyers ready for homeownership.

“From grants to forgivable loans, down payment assistance is the largest category of programs we track. This gives buyers flexibility when it comes to applying for down payment and/or closing cost help,” said Rob Chrane, CEO of Down Payment Resource. “Buyers should discuss their program options with their loan officer and real estate agent to make sure they choose the program best suited to their personal needs.”

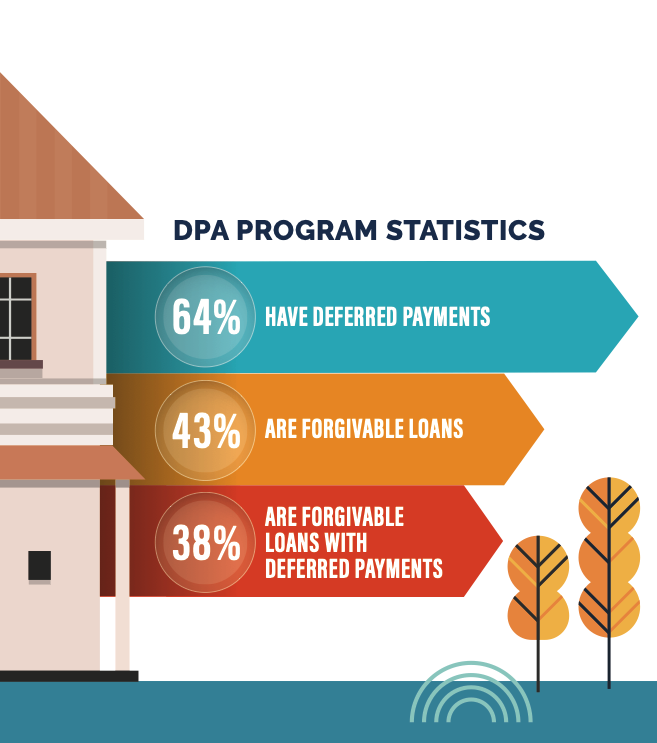

Some accrue interest, while others are amortizing loans. They typically range from 5-year to 30-year loans with varying payback provisions. The repayment may start immediately or kick in after a predetermined period of months or years, referred to as a “soft” second.

The GC97 Freddie Mac HFA Advantage Program with GC97 Plus, offered through the Tennessee Housing Development Agency, is an example of a soft second. Buyers can receive up to $7,500, depending on the sales price of the home. The loan is amortized over a 15 year term, and the interest rate is the same as the first mortgage.

Some repayable programs have a partial balloon payment, where the remaining balance of the original second mortgage will come due at the end of the second mortgage term.

With a silent second or deferred loan, payments are postponed until one of several events occurs—usually, when the borrower sells, refinances, rents or moves out of the original home purchased.

These loans are ideal for buyers who plan to live in the home for several years, so they can benefit from the home’s appreciation in value. However, there could be a 1099 coming in the mail after the buyer sells, refinances, rents or moves out of the home—a taxable event buyers need to be aware of and plan for.

An example of a silent second is the Florida Housing Finance Corporation Florida Assist program, available statewide. This program offers buyers up to $10,000 for Government loans and up to $7,500 on Conventional Loans. The payments are deferred, but the loan will be due upon sale or transfer of the property, satisfaction of the first mortgage, refinance, or a change in occupancy.

With a forgivable second, some or all of the original down payment assistance amount is forgiven. When and how much will vary, but it’s common for a percentage of the loan to be forgiven each year for a predefined number of years. If the program’s conditions are not met—for example, the buyer moves out of the home—the loan must be repaid, at times with interest.

One example is the New Mexico Mortgage Finance Authority HOMENow Program, available statewide. This second mortgage provides the lesser of 8 percent of the sales price or $8,000 to first-time buyers and can be used for down payment and/or closing cost assistance. The program is non-amortizing, has a zero percent interest rate, and is forgiven after 10 years, if the borrower meets the program provider’s requirements.

Grant programs do not incur a lien on the property being purchased and have no associated note or deed. These programs offer a true gift to the buyer at closing to help cover the cost of some or all of the down payment or closing costs and provide immediate equity.

The PenFed Foundation Dream Makers Grant is a national grant program that provides eligible military or veteran homebuyers with a 2-to-1 matching grant up to $5,000.

73 percent of programs in the database are for down payment or closing cost assistance.

11 percent are additional programs, including matched savings programs and Housing Choice Vouchers (HCV).

10 percent of programs are first mortgages.

5 percent of programs are Mortgage Credit Certificates (MCCs).

Download the press release and full infographic.

Never want to miss a post? For more useful down payment and home buying information, be sure to subscribe to our mailing list.

Are you an industry professional? Download our latest Down Payment Report for the data and news on first-time homebuyers and residential down payments.

Have a success story to share? Please contact us at info@downpaymentresource.com.